N

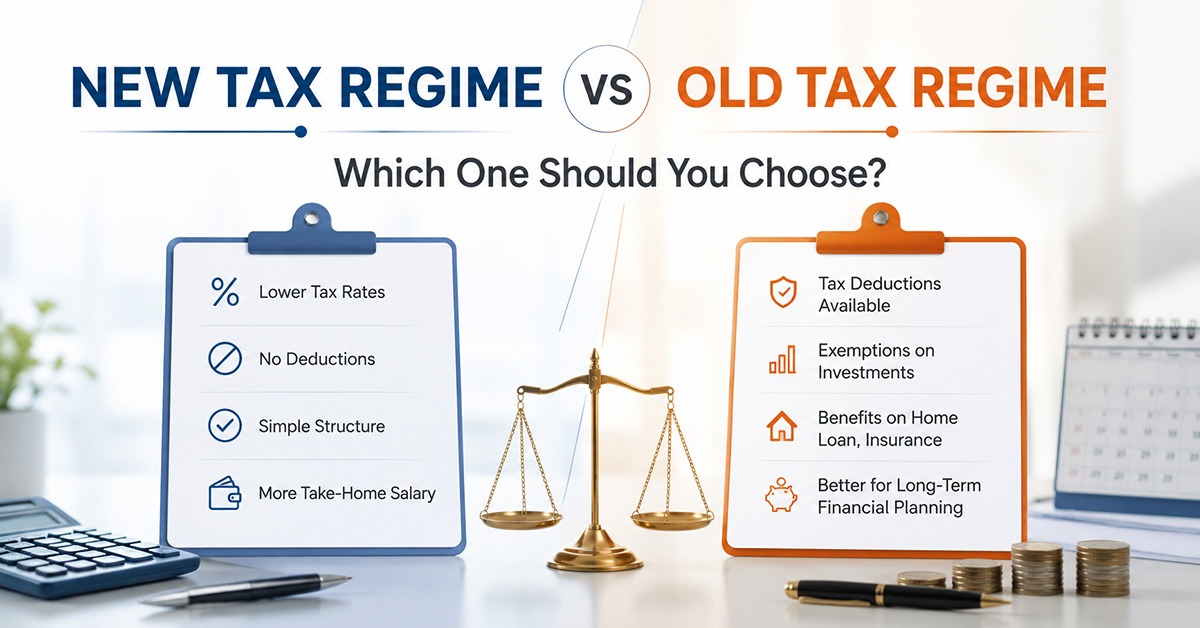

The Indian government threw a curveball in 2020: a new tax regime with lower rates but fewer deductions and exemptions. It's a bold move, aimed at simplifying tax filing. But did it really simplify things, or just add another layer of confusion for taxpayers? Choosing between these two isn't straightforward, especially when both options seem to pull you in different directions.

The Basics of Income Tax Slabs

Before diving into the differences, let's understand the basics. India's income tax structure is based on slabs — the more you earn, the higher the tax rate. Under the old regime, deductions and exemptions like Section 80C, HRA, and others allowed taxpayers to reduce their taxable income. The new regime simplifies this by offering lower tax rates but cuts out most of these deductions.

Here's a glimpse of the current slabs:

- Old Regime:

- Up to ₹2.5 lakh: Nil

- ₹2.5 lakh to ₹5 lakh: 5%

- ₹5 lakh to ₹10 lakh: 20%

- Above ₹10 lakh: 30%

- New Regime:

- Up to ₹2.5 lakh: Nil

- ₹2.5 lakh to ₹5 lakh: 5%

- ₹5 lakh to ₹7.5 lakh: 10%

- ₹7.5 lakh to ₹10 lakh: 15%

- ₹10 lakh to ₹12.5 lakh: 20%

- ₹12.5 lakh to ₹15 lakh: 25%

- Above ₹15 lakh: 30%

The Allure of the Old Tax Regime

The old tax regime has its loyalists. Why? Because of the deductions and exemptions. For those with home loans, investments in PPF, LIC, and other instruments, this system offers significant tax savings. For instance, under Section 80C, you can claim up to ₹1.5 lakh, which can substantially lower your taxable income. Add medical insurance under Section 80D and interest on home loans, and the benefits stack up.

But there's a catch. The old regime requires meticulous planning. Each investment or expense must be documented and often declared in advance. It's a system that rewards the disciplined and punishes the forgetful.

The Simplicity of the New Tax Regime

Enter the new tax regime: a breath of fresh air for those who dread paperwork. No more hunting for receipts or grappling with fine print to maximize deductions. This regime, with its lower rates, appeals to those who prefer straightforward calculations. It's especially attractive for younger earners who may not have significant investments or home loans yet.

However, its simplicity is double-edged. By opting for it, you forgo a slew of deductions and exemptions. For some, this trade-off might mean paying more tax than under the old regime.

Making the Choice: A Personal Decision

Choosing between these regimes isn't just about math; it's about life choices. Consider a 30-year-old single professional, earning ₹12 lakh annually. Without major investments, the new regime might save more taxes upfront. But for a 45-year-old with children, a home loan, and hefty insurance premiums, the old regime could offer substantial savings.

It's also about flexibility. The old regime encourages saving for the future, while the new regime offers more liquidity. If you're someone who prefers spending or investing outside traditional tax-saving instruments, the new regime could be your friend.

Crunching the Numbers

Let's crunch some numbers. Suppose you're earning ₹15 lakh annually:

- Old Regime:

- Taxable income after ₹1.5 lakh Section 80C deduction: ₹13.5 lakh

- Tax: Approximately ₹1.91 lakh (after accounting for other possible deductions)

- New Regime:

- Taxable income: ₹15 lakh

- Tax: Approximately ₹1.87 lakh

At first glance, the new regime looks cheaper. But factor in other deductions like HRA, medical insurance, and interest on loans, and the old regime could pull ahead.

Tax Planning Strategies

Tax planning isn't just about choosing a regime; it's about aligning with your financial goals. Consider:

- Life Stage & Goals: Young professionals might prioritize liquidity, while those with families might focus on savings.

- Investment Appetite: If you're investment-savvy and disciplined, the old regime could be more beneficial.

- Salary Structure: Your CTC breakdown could influence which regime is more advantageous.

Something to Ponder

Here's a thought: the new regime, in its quest for simplicity, may inadvertently encourage consumerism over saving. By removing the incentive to invest in certain government-backed instruments, it could shift spending patterns. Is this a subtle nudge towards a more consumption-driven economy?

FAQs

Which tax regime is better for a salaried individual?

There's no one-size-fits-all answer. For salaried individuals with substantial deductions and exemptions, the old regime might be more beneficial. However, if you prefer simplicity and have fewer investments, the new regime could save you more.

Can I switch between the old and new tax regimes?

Yes, salaried individuals can switch between regimes annually while filing returns. However, individuals with business income need to stick with their choice until they no longer have business income.

Is the new tax regime beneficial for those without investments?

Generally, yes. If you don't have major tax-saving investments or loans, the new regime's lower rates could be more advantageous. Yet, this depends on individual income and expense patterns.